Podcast: Ep.6 The Different Styles of Top Investors and Traders (Value, Growth, Discretionary, and Quantitative)

Many of us have heard of the big name investors and traders out there, but what makes them different? What styles do they use? How do they approach markets? What separates the best from the good? This episode is an intro into the different type of investing and trading styles, so you can find one that best suits you. This will help separate some of the confusion when you see “value” and “growth” funds or when reading about discretionary and quantitative traders. We conclude with a discussion about how the top traders approach markets.

With that! Here are the links. If you have iTunes please use that as it helps my rankings within the store. Don’t forget to subscribe to stay updated on future episodes!

You can find the script of this podcast at the bottom of the E-mail.

Supplemental Information:

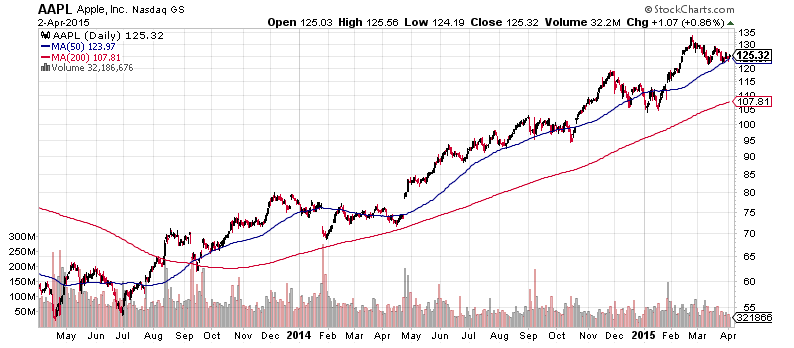

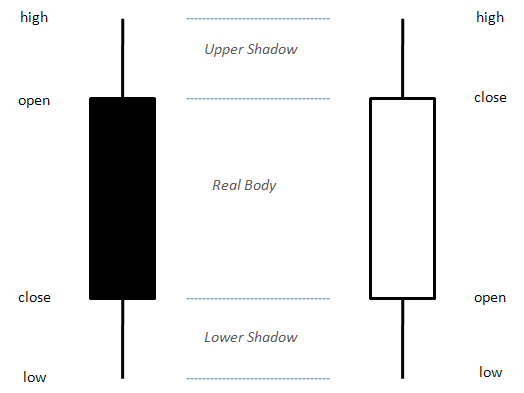

The picture above shows an example of what a candlestick is when looking at prices on a stock chart. The chart below uses candlesticks when showing the prices of AAPL

The picture above shows the simple moving average technical indicator. It’s a rolling average of the past 50 days and 200 days (SMA 50 and SMA 200 respectively). The SMA 50 is in blue and is quicker to react to recent price changes. The SMA 200 is in red and is a longer-term indicator so it is slower to react to recent price changes.

Here is the script that was used in today’s episode.

Note: I don’t follow scripts word-for-word as they can sound unnatural, but the episodes do closely follow them.

How many types of investing and trading are there??

Welcome listeners to episode 6. Have you ever wondered what people mean when they say, “I’m a value investor.” or “I use technical analysis?” Some might say, “I’m a momentum trader” or “I trade special situations.” For my regular listeners, you know I’m not just going to define things, that’d be too easy, but I’m going to expand upon them, give some of my experiences, and shed some light on different perspectives. This is going to be important if you have an interest in picking stocks or even mutual funds, index funds, and ETFs. Many different financial products advertise themselves as using particular type of investing or trading style. And as usual, you can see the script of this podcast online at blog.tiingo.com if you want to follow along.

Before I begin there is one thing I need to discuss. You can skip over the next few minutes if you decide, but given how much time we put into this podcast, both us creating it and you listening, it would mean a ton to me if you could listen to the next few minutes.

I left my job trading professionally a year ago, I didn’t know what I wanted to do. Strange, right? I left a great job where I was doing well, the first employee of a hedge fund that grew 5 fold in a year, and on a whim I left. Well, I didn’t really leave on a whim. The reason I left is that something inside of me wanted to do more. Over the past few years, I saw many people lose money to misinformation. I mean it’s nobody’s fault. It’s strange isn’t it? Our whole lives we learn things like writing and science, but nobody teaches us finance. Then, suddenly when we get our first job in our 20s or 30s, everybody is telling us to invest it. For those of us fortunate enough to have 401ks or be able to contribute to IRAs, suddenly it’s people telling you “put this in mutual funds! or put this in index funds!” But wait, who taught us any of this???

This would be like never taking a history class from 1st grade through high school, then the day after graduation saying “write a paper outlining the American Revolutionary war.” Wait, what? This is what financial education is today – non-exist. And this is where Tiingo has stepped in fill the gap.

This podcast promote education and financial literacy. And not just the basics, soon this podcast is going to touch upon very advanced stuff, but I promise you will be able to follow along. Alongside this, I built tools that allow people to use this education to better their portfolios. I continue to build them and I find more and more users are using them are listening to this podcast.

Tiingo’s intention has always been to help people. I always figured monetizing it would figure itself out. But the reality is, I’ve spent the past year building Tiingo and this podcast out of my own savings, and for this to continue I simply ask you pay what you feel. Even if it’s $2 dollars a month, less than the cost of a cup of coffee…or $5 the cost of a latte. Whatever you feel is appropriate or can afford to pay, I ask that you do so I can continue this. You can do so at Tiingo.com/support. That’s t-i-i-n-g-o.com forward slash support. The tools are will be free so if you can’t afford or don’t want to pay, still feel free to use the site. I don’t believe in showing partiality between those who can pay and those who can’t. You will always know your situation better than I. But, Tiingo’s mantra is “Actively be good.” A famous mantra in tech by Google is, “don’t be evil.” But the financial sector needs to be stronger than that. We’ve violated the trust of people, and because of that, the mantra for Tiingo is always going to be more active, so we have the mantra as “Actively be good.”

So like I said, if you want to support the Tiingo mission, community, web app, or podcast, please consider paying what you feel at http://tiingo.com/support.

With my heartfelt message aside, let’s get into some investing and trading fun! Woo Woo!

So you’re now thinking, “Rishi I think I got the basics down and some more…but what else is there.” This is the perfect podcast episode for you. We’re going to discuss the differences between investors and traders and then dig into the different styles. There are many ways to make money in markets, and you often see the news media discussing certain individuals. A lot of these individuals tend to stick to a particular type of trading or investing. For example, Warren Buffett is the most well-known, and richest value investor –a term we will explore later.

This way, if a professional trader or investor recommends a stock, you will have a better idea where they’re coming from. This will be important as some of you may hear a trading or investing style and be put off by it. It’s interesting how the way you invest or trade reflects personality sometimes. You have those who are very relaxed long-term, then others who are constantly moving and taking action.

To begin, let’s go ahead and start off with the basics – what is the difference between an investor and trader. Once we do that, we’ll start getting into a lot of the different kinds that exist and taking it to a further level than your traditional book. As usual, we will always start with the basics and build our way into mind-blowing stuff. Just a heads up, I’ve spent a lot of time thinking about this topic. It’s sort of a philosophy I hold, so you may find these definitions different than what other sites say. I will explain why I think the ones presented here may be a more accurate representation.

The traditional thought is that investors are long-term buy and holders. They are in a company because it is fundamentally a solid company. What I mean by that, is that each publicly traded company is required to publish accounting statement. What investors often do, is that they consider the company’s business prospects, and the sector they are in, then they look at the account statements to verify the company has solid business prospects. They consider them stakeholders in the company and typically have time horizons 5 or more years out. They don’t worry so much about the next month or so, unless something drastic happens, but expect the company to outperform in the long run.

What does this all mean? Investors treat companies they get in like a business. Let’s say one of your work colleagues comes to you and says, “Hey I want to start a restaurant business, lemme get some of your money.” I’m not sure about you, but if one of my work colleagues, whos been a programmer his whole life tells me he wants to start a restaurant I’m not gonna give him money off the bat. I would want to make sure what he brings for lunch looks delicious first of all.

Ha, no but in all seriousness, while you may know the individual, if he asked you to become a partner and own 50% of the restaurant, you would start making sure it was a good investment. You may look at where the restaurant is, what it sells, how good the food is, whether or not it’s in a good location, and so on. You would want to make sure that it’s a good business. You may even want to look over the balance sheet of his other restaurants to make sure there was no fraud in the past and so on. This is how an investor sees a business.

Sometimes it can be tough for us to conceptualize because we’re so used to seeing prices on a screen and trading on them, we don’t really think about the accounting behind the firm or its prospects. Warren Buffet is the most well-known example of a long-term investor. When he puts money into a company, he doesn’t have an end date.

Now most of us may be thinking, “well of course, when Warren Buffet buys shares he ends up owning a huge percent of the company.” While that’s true, and companies sometimes hook him up with favorable deals because of his reputation, that doesn’t mean we shouldn’t take his same perspective. When you buy shares, you are owning a business. It’s a fact and it’s an awesome concept.

Now there is one thing that can make owning shares better than investing in your friends restaurant. And that’s the concept of liquidity. Liquidity is a financial term that means being able to convert any asset you own, stocks, a house, even your laptop, into cash. Your laptop may be less liquid, as well as your house, but stocks can be seen as very liquid most of the time. You can simply go to your stock broker, sell your shares, and viola you no longer own the business (once the transaction clears). Try doing that with your friend’s business! To recap, investors treat buying shares as owning an actual company.

Also just a quick aside: I said stocks are liquid most of the time. Sometimes they are not if there aren’t many shares issued, or if volatility is high. During times of panic, liquidity can fall because people are not sure what to do. Uncertainty can reflect itself in volatility, as mentioned in the last episode, and also result in lower liquidity.

Okay onto traders:

We are now about to enter some blurred lines between investors and traders. Sometimes there is no clear cut definition and I’m going to try my best to show why. Technically, when an investor buys or sells shares, they are trading stocks, ETFs, mutual funds, or so on. This is why it gets confusing. Technically a trader is somebody who trades an asset. But this is a technical definition and isn’t really helpful to us when we’re trying to learn about different styles.

When you hear trader in the media, it means something different than the technical definition. And this is the type of trader we’re going to talk about going forward.

A trader looks at a stock as something that has a defined end date. When they enter a position, they have a clearly defined rule for when they get out. Some of my listeners may claim that this is a pretty strict definition of a trader. A lot of long-term investors have criteria for when they will get out of a stock or investment. And this is true, but here is where I will argue the difference lies: a trader trades a position with the intention of them knowing they will get out eventually. An investor enters a position without the intention of getting out, but they accept as a business changes it may no longer be a good investment.

I know you may be wondering what the difference is, and this is why the definitions can be so blurry.

Let’s say your friend who wants to open a restaurant checks out. He is an amazing chef. He found a way to put chocolate on a savory pizza and make it the best thing you’ve ever eaten. Wow, I just cringed at that, but I’m sure somebodys done it.Anyway, when you’re giving money to your friend as an investor, you’re not thinking, “Ok I’ll give him money, make a ton of money, and get out like a year from now.” You may think, “Ok I’ll give him money, his business idea seems legit, and I think he will be successful. If he isn’t successful, or if he goes off the deep end, I’ll re-evaluate and may pull my money out.”

If you were a trader, you might think, “Okay the quirky pizza market is so hot right now. It’s like the new up and coming food, like what artisan cupcakes once were. I’m gonna give him money, and pull out 2 years from now when I think the quirky pizza market will top. Then I’ll make the most amount of money”

That’s the difference – the intention of you as a shareholder! One sees it has a business opportunity, and the other sees it as an opportunity to express a viewpoint you have

Here’s why the intention matters so much: it’s really the only way to separate the two. Some traders look at companies balance sheets, some hold positions for more than a year. Traders are often typecast as individuals who are in and out of positions very quickly. But such a huge variety of styles exist, that I’m putting forth an idea that what really separates a trader from an investor is their intention when they place a trade. One sees it as a business, and the other sees it as an opportunity to capture a recent view they have on markets.

With the differences established, let’s move forward:

Let’s discuss the different types of investing. This is gonna be fun. So many of us read about these amazing investors, but what we often don’t hear is the styles of traders. As I said earlier, there are so many different styles that reflect different personalities. In this episode, we’re going to describe some of the most common because a lot of mutual funds and ETFs were created to try and replicate these styles.

The first thing we will explore is one of the most common: value-investing.

The most famous value investor is Warren Buffet. The premise behind this style is that you think a company is undervalued. For some reason, the market is undervaluing this company. This is because you looked at the account sheets, otherwise known as doing fundamental analysis. This is often combined with something else, but before we move onto that something else, I will explain a common concept value investors use.

And that is the book value. The book value is what a company is worth if you take the assets and subtract the liabilities. What I mean by that is imagine everything a company owns. The building, the computers, the technology, the patents, how much cash it has, what investments it has (like stocks), and so on. These are the company’s assets. Now thing of all the loans it owns, who it needs to pay money to and so on. Those are the liabilities. So if you take all those assets, and subtract the liabilities, you get how much the company is worth according to its books, or the book value. So if a company has $200mm worth of assets, and a $40mm loan, its book value is $200mm – $40mm which gives $160mm. That number, the $160mm is the book value of the company. So now that we know what the value of the company is from an accounting standpoint, or the books standpoint, we need to see what the market thinks it’s worth.

So we have to calculate something called the price/book ratio. First, since a company is broken up into many different pieces, or shares, we take the book value and divide it by the number of shares. So our book value was $160mm, and let’s say the company is broken up into 1,000,000 shares. That means each share represents $160 of book value. In other words: If the company is worth $160mm according to the accounting statements, and there are 1,000,000 pieces, then each piece is worth $160.

Next, we can see how much the market prices each share. For that, all we have to do is look up the stock price. So let’s say the stock price is $80/share. Whoa! If we closed down the company, sold off all its assets, paid its loan, we would have $160 a share! Yet the market is only selling it for $80/share! A value investor might immediately buy the stock because they think, “Once the market realizes how undervalued it is, other investors and traders will buy a ton and the price will get to $160/share.”

A common metric to look at is the price/book ratio. You take the market price of the stock, divide it by the book value per share, and that gives you the price to book ratio. In this example, it would be $80/share divided by $160 book value per share. This creates a price/book ratio of 0.5.

This situation vey rarely happens. Typically you see price/book ratios of 2 or greater. But let’s say you do see a P/B ratio of 0.5. Typically this will happen if there is something else the market thinks will happen. An accounting statement is typically released once a quarter, or once every 3 months. In those 3 months, something could drastically change. For example let’s say we’re an oil company and we make a lot of money from selling oil. What if in the past 3 months, Oil dropped from $100/barrel to $50/barrel? Well our business would probably be worth less, so the market is taking that into consideration. The accounting statements wont take that into consideration until the next time they’re released. This is often referred to as lagging data.

SO if you are seeing a P/B ratio of less than one, be skeptical. It could be the case that everything is okay, or you think it’s still undervalued, maybe not as much as the P/B tells you, but maybe the market overreacted. And this is the job of the value investor. To not only look for things that are undervalued, but also to figure out why, and whether or not those considerations make it less attractive.

P/B is just one metric value investors look at. We will cover more metrics and what these accounting statements mean in a future episode. There are text books written on this topic, and given the limitations of this podcast, we can’t properly cover the topic in one episode. But this is the basic idea behind value investing. You buy things that are undervalued, or in other words, you buy things that are undervalued.

A major drawback to value investing is that you assume the stock price will eventually accurately reflect what your think it’s worth. Often times, stocks may not do that or the price comes down even lower. Sometimes the markets, or other investors, have their own train of thought. Also in a crises period, something may look cheap, but because of panic selling, correlation among stocks becomes higher. In other words, the stocks move up and down together regardless of how good or cheap a company is. Especially during those times, buying something that’s a value could mean the stock continues to go lower because of issues outside the company, like a recession. So always be careful if something looks cheap. Ask yourself why? There may be a reason why the rest of the market thinks the company is worth much less than our personal analysis may show.

The next type of common investing is called growth investing:

Growth investing is a type of investing where you expect a company to rapidly grow in earnings or the potential for future earnings. The premise is easy to understand, but implementing it is a very difficult idea. Many different investors have their own type or measure of criteria for detecting what makes a rapid growth stock, but the general consensus is that you expect the stock’s earnings to grow at 12% or higher a year. Often times if a stock is growing too rapidly though, it could mean management may be getting to aggressive or reckless. They could be taking a lot of loans to achieve that earnings growth.

Everything in moderation.

The biggest issue with growth stocks is that we just can’t predict the future. How do we know a company is going to continue growing? What if people stop liking it or it falls short of expectation? When we think something continues growing, we often have to consider a lot of assumptions have to be made to make that prediction.

For example, if our friends pizza place turns out to be growing rapidly, everybody loves chocolate savory pizza, then our friend may continue to grow. We are excited because at this rate we will be so rich! But wait, what if this pizza has tons and tons of gluten and suddenly the entire town goes gluten free? Your friend tries making a gluten free crust, but it just doesn’t taste the same. When we assume the growth will continue, we’re assuming a lot of things. In this case we assumed the pizza audience stay the same and maintain the same tastes, same ideas of health, and same desire to get pizza.

With investing, just like when buying a business – they’re the same thing really, we make a lot of assumptions. Whether we think the price will go up or the conditions leading to that businesses success will stay the same.

The reason I bring up growth and value investing first, is because these are the two most common types of investing. You often see mutual funds, etfs, and even some index funds that have some sort of value or growth stock picking strategy. I say even index funds, because they are seen as following a basic index. Often times they will follow an index but a bit more capital on stocks they think are high value or high growth. Every mutual fund, index fund, and etf is different on how they do this.

The next disclaimer I want to make is that the line between value and growth is actually not so clear cut. Often pooled investments like the mutual funds, index funds, and etfs mix a blend of growth and value. And while many people consider Warren Buffett a value investor, he doesn’t. He consideres himself a value and growth investor and argues that they’re really not that different. His process uses both and he thinks they are interrelated.

A general theme you will notice among investors and traders is that they often blend different styles to create their own. This also often reflects personality and what appeals to them. Think of it as sort of your political view. It’s not common to have a view that’s 100% the same as your political affiliation. There may be issues that you agree with different political groups on.

Let’s focus on some different trading styles

A common stereotype is that investors focus primarily on the fundamentals, or accounting, along with other market conditions, and traders focus on something called technical analysis. The truth is that many mix and match their styles. If you want to learn more about this, I strongly recommend you read Market Wizards, all four of them, and in particular the first two. It’s an interview style series of books that talks to the top traders of a few generations now. It’s an incredible way to learn how some of the top minds look at markets and the backgrounds. It’s very entertaining and easy to read. I highly recommend the book series to anybody trying to learn more.

But let’s discuss what technical analysis is.

Technical analysis is the idea of looking at price, volume, and other historical market data to predict the future. Well, that actually might be the technical definition, but I’m going to expand upon this and say while technically technical analysis tries to predict the future, we have to be careful the way we say predict.

Here’s why: when technical analysis do their work, they aim to be right half the time. Some of the best traders will have hit ratios, a ratio of the # number of winning trades to the # of losing trades, of like 55%. That’s pretty much only half. So when they predict the future, it’s not with 100% certainty, it’s trying to be right more often than they’re wrong. This is actually true of all traders, not just those who use technical analysis.

And here’s another twist: sometimes traders don’t mind being right less than half the time. But how do they make money? Sometimes traders bet that even though they lose more times than they win, when they do win they win big enough to make up for the losses.

So what’s example of technical analysis? One of the most common is the idea of the “golden cross.” It requires doing a simple moving average, or SMA. That is for each day, you take the average of the past x number of days. For example an SMA 50, is a simple moving average of the past 50 days. This captures the general price trends, it “smooths things out.” I put a screenshot on the blog of what this looks like, look for the podcast episode 6 blog post. So the golden cross is when the SMA 50 crosses above the SMA 200 you go long. In other words, when the short term trend, SMA 50, breaks the longer term trend, the SMA 200. There is a picture of this on the blog too. But the idea is that the shorter term trend crossing the longer term, means things are starting to look up and it’s time to buy. This strategy tends to work when things are trending, but works terribly if stock prices aren’t going up but moving in a range.

There are thousands of different technical analysis tools, but the question you may all be asking is, “Rishi, does technical analysis work.” I’m not going to back down from this question. This is a hot debate among many people and I will say this: yes, but not in a way many people use it.

The best people I’ve met who use technical analsyis, and keep in mind I am considering all historical market data when making this claim, do not use it in the way that many books teach it. They do not look at candlesticks and think, “this has to happen.” The best traders I know who use it, see it as a framework to look at the world. They use it to compare current events to previous. They understand that it doesn’t work all the time. And they understand that in certain market cycles it works, and in other market cycles it doesn’t work. For a ten year period the strategy may not work, but the next 10 years it may work wonderfully. They spend their time trying to understand why it works and when it works. They spend their time making sure it’s not just randomness.

Some technical analysis traders use computer programs to execute trades quickly. Some academic paper show it works, but not extremely well like you may think. If you’re scanning academic papers, look for things like momentum strategies. Often times they use more advanced concepts like portfolio construction to boost returns, this is a topic we will cover later.

What really upsets me is when I read books like “You can make millions by learning these patterns.” No, that’s a sure way to lose money. The best technical analysis people use very few indicators and don’t clutter their screen. They prefer simplicity not complex models. There is a good mathematical reason for this, why simple is better, that we’ll touch upon in a future episode.

If technical analysis was perfect, everybody would be doing it. It takes a lot of hard work, thousands of hours to get right, and even then success isn’t guaranteed.

There are many ways to make money and it’s not an easy problem to solve. Often times a lot of books and research market technical analysis to beginning investors and I can’t stand this. They make it seem like it’s a get rich quick scheme. They don’t include things like statistics, how many strategies don’t really work, and how it’s an extremely complicated problem. As a new investor or trader, I can’t stress enough that you don’t trade real money with technical analysis. And a lot of marketing material promises riches for following a new technical analysis system. Any time you see a publication telling you this stock trading robot made a ton of money, always wonder why they wouldn’t keep it a secret? Why wuldn’t they just trade it for themselves. In markets, if a strategy that generates a lot money is made public, it stops making that kind of money. The reason? Once people know what a strategy is, they put the bets on before anybody else.

Think of it this way, if you knew this stock robot made a ton of money and what it was going to buy, wouldn’t you buy it first? And if everybody bought it, the price would go up too much, and so you would have others selling it. It’s a complex topic we’ll touch upon in a coming episode about market theory, but when a money generating algorithm is creating, you keep it a secret. As soon as other people in the market figure it out, they will place the trades ahead of you and if you were planning to buy the stock at $80 and sell at $90, because other people bought it before you, it’s now at $90 and your trade makes no money. In fact, some people will start purposely selling it at $80 because they know there will be buyers, and as soon as the price doesn’t go up, the buyer realizes the strategy isn’t working, then sells it. Now you have a ton of sellers. And now the people who were originally selling? They are now buying again because the price has come down a ton. This is how secret strategies break. So if somebody is promising you an amazing technical analysis strategy, know that there’s almost a 100% guarantee it’s a sham.

Before I conclude this section on trading, I want to discuss two types of trading you hear about: discretionary and quantitative, and the stuff in between

One type of trader you hear about is the discretionary trader. At the extreme end of the spectrum, they are traders who trade on gut feeling, but there is much more to that. The successful ones have been watching markets for many many years and constantly pour themselves into research and sometimes technical analysis studies. They read history books understanding what happened at different points in time and are constantly keeping up with the news. While they do follow risk management and don’t take positions that are too big, they don’t automate this process. They believe their mind allows them to quickly adapt and understand when markets change. This is their edge.

Quantitative traders at the extreme end are those who completely automate their process. They research markets, constantly test strategies…some strategies may be technical analysis based, others may be news reading algorithms that take positions before anybody else can, and when they get a signal to buy or sell, an algorithm takes care of it. Quantitative traders can be highly quantitative in that they look at markets in statistics or a programming problem, while others believe they can use market events and economic trends to create a system.

Most traders often are a blend of the two that fall somewhere on the spectrum. Some may have algorithms but sometimes exercise discretion on them. For example if an algorithm is telling them to buy, they may realize the algorithm doesn’t take into account information it hasn’t seen before, so they will decide not to do it. After speaking with many people, some traders argue that the best traders are those who take into account both quantitative and discretion. My opinion?

It doesn’t matter. The best trading or investing style will be what works for you and what fits your personality. It will take many years and thousands upon thousands of hours worth of work. People often think of wall st or investing and trading as glamorous jobs…but in reality the top traders I’ve worked with constantly pour themselves into their work. They do it because they love their job, not necessarily for the money or lifestyle. In fact, the top traders I know you would walk right by on the street and never know. For them this is what they love and they spend much of their free time doing it.

Actually, you know what – I’m going to conclude this episode now by telling you the secret of the greatest traders and investors I know. I’ll say it multiple times throughout this series, but I need to declare this right now because trading and investing can often be an art and takes work. So here’s the key before we continue: the best traders and investors are those who view their style as a process. A process they are constantly improving and making better. They know eventually the outcome will follow, but at each step they are studying their mistakes and winners. They realize that their outcome is a mixture of skill and luck. They can’t control the luck, but given enough time, the skill will win out. They keep journals of their winners, losers, and what’s going on in markets. They are generally nice people, humbled many times by getting their butt kicked in markets. Yes, you hear of the ones who are jerks, but jerks who are successful aren’t as common as it appears. Many have a philosophy behind doing what they do.

So becoming a good investor and trader is a lot of hard work. You hear of the people who start immediately and get rich, but many of them are lucky and do not last long. It takes a lot of grit and hard work, which is in my opinon why you often see traders who are very humble. Unfortunately, the ones who are not so humble often make themselves shown on TV.

Oh man, this kinda feels a little motivating. Don’t be intimidated by the hard work. In fact, embrace it. Because if you embrace it you have a two options 1) you can decide to put in the effort to constantly get better or 2) you can decide it’s not worth it for you and you rather be more passive or laid back about your investments. Both are good options and it depends upon your personality.

If you decide even on #2, this podcast will continue to be helpful for you because the types of stuff I’llb e discussing are for those who want to trade or invest actively, and those who want to do so passively. Many of the same tactics to improve portfolios work on both types of traders. They’re some really cool concepts we’re going to discuss and I’m excited. Knowing about the different types of investing styles really opened my mind to markets.

A lot of people don’t typically see financial markets as a creative space, but it really is. I mean, you have to not only be creative to come up with cool ideas many people haven’t though of, but also you have to have courage and discipline. A lot of traders and investors find ways to generate ideas. They love it. You could be walking through the streets of a city or a mall and suddenly see a new store or restaurant. You may eat the food and love it, and now you want to know if it’s a good investment. Maybe it’s only the 12th store open but the company trades ona s tock exchange. Once you start investing and trading, you see the world filled with opportunities and your brain will constantly be coming up with new ideas.

My goal in this series is to help you get your ideas into your portfolio in the best most possible way. Maybe your ideas lead to index funds of stocks and bonds, but even in that space there is so so so much you can do to improve even the most passive of portfolios. I can’t tell you all how excited I am.

Okay all, hope you had as much fun listening to this episode as I had creating it. Please E-mail me with feedback at [email protected]. If you have any questions, E-mail me as well and I’ll do my best to get back to you. I sometimes send ridiculously long E-mail replies back to people, so I may start institution a 15min call to discuss with you an answer instead haha. Anyway, please support Tiingo so that I may continue doing this. The site to send a few bucks, even $2/month, is Tiingo.com/support. Thanks so much and will be back soon! I’m going to be working on an episode with Brett Harris about student loans. It will be good, so get ready.